Are you an artist receiving secondary sales? Saim explains why your NFT Artist Royalties are considered active business income in 2026 and why the IRS requires them on Schedule C instead of Schedule E. Learn how the 15.3% self-employment tax applies to your “passive” NFT Artist Royalties and what you need to do to stay compliant in the era of high-fidelity blockchain tracking. Master your NFT Artist Royalties and protect your business.

Key 2026 Reporting Facts:

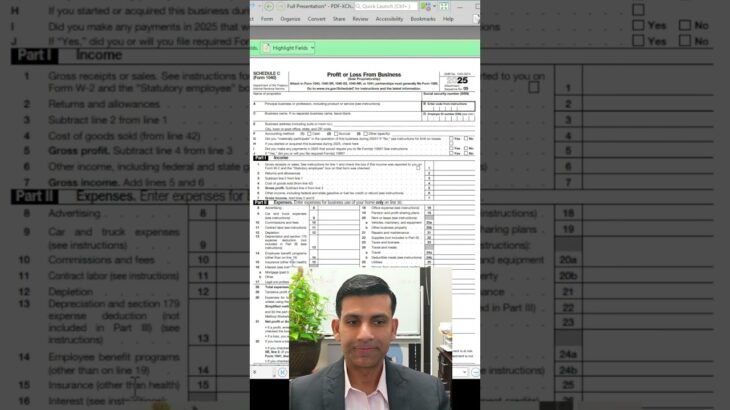

NFT Artist Royalties are ordinary income for creators.

Active work in a trade or business requires Schedule C.

These royalties are subject to Self-Employment Tax.

Failing to report NFT Artist Royalties correctly can trigger automated audits.

Contact our team at:

info@akifcpa.com

Visit Our Website:

www.akifcpa.com

Full YouTube Video:

Follow for more:

https://www.youtube.com/@saim.cryptocpa

https://discord.gg/Z5YQKRDB

https://www.instagram.com/saim.cryptocpa/

@crypto.cpa

https://www.linkedin.com/in/saim-akif/

Call Us On:

US (713) 451-9700

CA (416) 800-2709

#NFTArtist #Royalties #TaxTips2026 #BitcoinTax #Shorts #Finance #AuditReady #CryptoCPA #TaxCompliance #WealthBuilding #FinancialReporting #ScheduleC #CreatorEconomy